March 12, 2024

Shifting strategies for retirement income

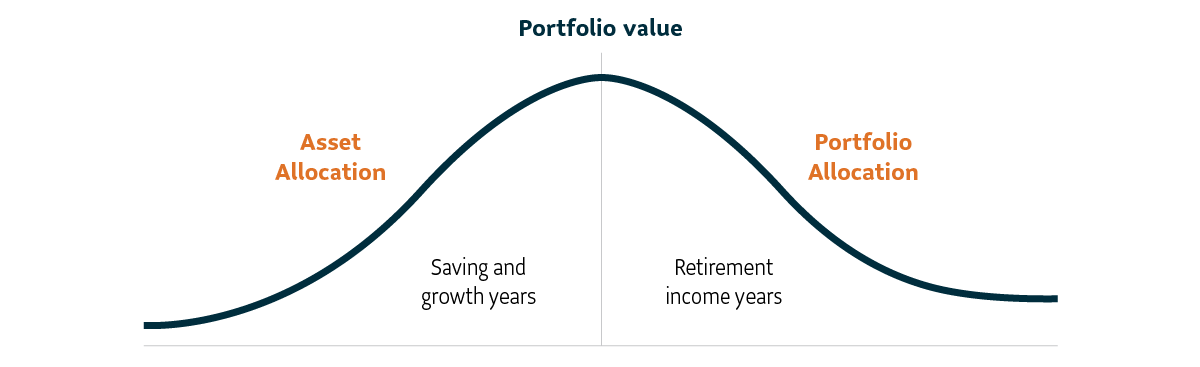

Moving from Asset Allocation to Product Allocation

Moving from Asset Allocation to Product Allocation

FOR ADVISOR USE ONLY

During a client’s accumulation years, the investment strategy you recommend likely includes Asset Allocation in some form. With this approach, you’re able to balance the client’s risk tolerance (using varying degrees of equities, fixed-income, and cash/equivalents) against their desire for growth and time horizon until retirement. But once a client nears or reaches the end of that time horizon and they retire, Asset Allocation may no longer be a strategy that serves a client’s needs. This is because the client must begin drawing an income from their investments. Further, this income must meet key retirement needs and address a set of risks that is unique to them.

An approach that can help accomplish this is called Product Allocation, also known as Income Layering. Product Allocation is the process of allocating (or layering) more than one income generating product into a retirement income portfolio in varying percentages. Each layer or combination of products has specific features and benefits that can address key retirement needs and compliment government benefits. Using more than one income generating product is critical because no one product can solve for all of a client’s retirement needs and risks. The goal of Product Allocation is to help ensure that a retiree’s unique needs, and the risks that are most concerning to them, are addressed.

What are considered key retirement needs and risks?

A fundamental requirement of a retirement income plan is to ensure a client’s basic expenses are covered. These expenses include, but may not be limited to:

Only once these basics are covered, can you focus on a client’s retirement lifestyle wants.

Longevity risk is the likelihood that a client could outlive their retirement income. With people living longer than ever before and increasing healthcare needs as they age, this risk is real. We now know that an income plan may need to fund a client’s retirement for at least 30-35 years1.

Market risk, or market volatility, is a concern in any portfolio. No one wants to see the value of their investments decline due to a market downturn. However, this is of particular concern to those nearing retirement and retirees at the start of their retirement. These clients, who are soon to begin drawing income or who have started to draw income, no longer have the luxury of a considerable length of time left in the market in order to recoup their losses. The risk of market losses just prior to or at the onset of retirement is known as sequence of returns risk, a subset of market risk.

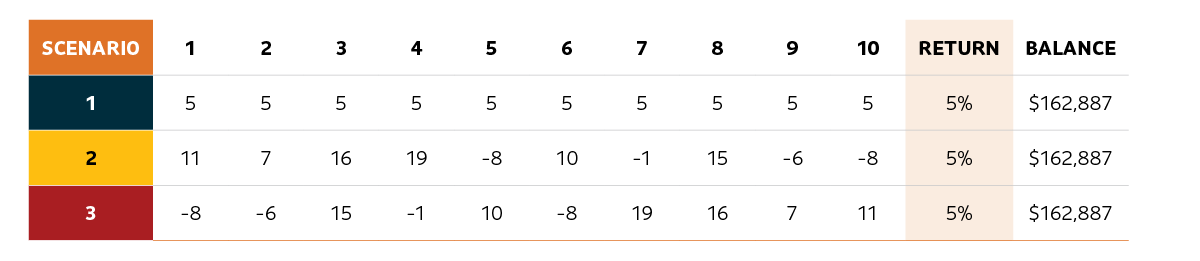

To illustrate how sequence of returns risk can affect a portfolio in the savings and growth years vs. a retirement income portfolio, let’s look at some scenarios.

Assumptions/parameters:

Exhibit 1 – the sequence of returns during the savings and growth years:

No money is withdrawn from any of the three scenarios. In scenario #1 (dark blue), the client earns a consistent return rate of 5% every year. With a $100K principal investment, after 10 years they have a balance of $162,887 in savings.

In scenario #2 (yellow), the rate of return varies from one year to the next, but most of the negative returns occur in the last five years. This scenario also has a balance of $162,887 after 10 years.

When we come to scenario #3 (red), the bulk of the negative returns occur within the first five years. Again, no difference in the end result: the client has a total of $162,887 – just the same as in the first two scenarios.

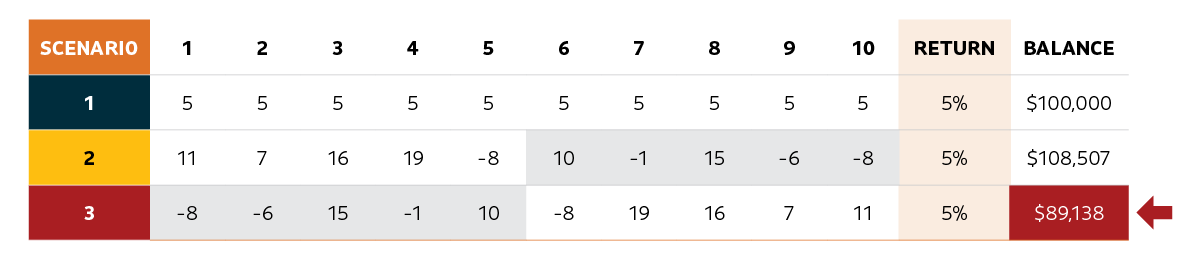

Exhibit 2 – the sequence of returns when drawing retirement income:

In Exhibit 2, however, look at what happens to the balances in scenarios 2 and 3 when the client is withdrawing 5% ($5,000 per year) in retirement income. In scenario 3, when the bulk of the negative returns occur in the first five years, they have $19,369 less than under scenario 2, where the bulk of the negative returns occur later on. This highlights that the sequence – or the timing – of returns makes a big difference when drawing retirement income.

And in scenario #3, given the client is drawing an income, it could be difficult for them to recoup the money they lost due to a market downturn. The client won’t have the luxury of a considerable length of time left in the market to recoup their investment losses.

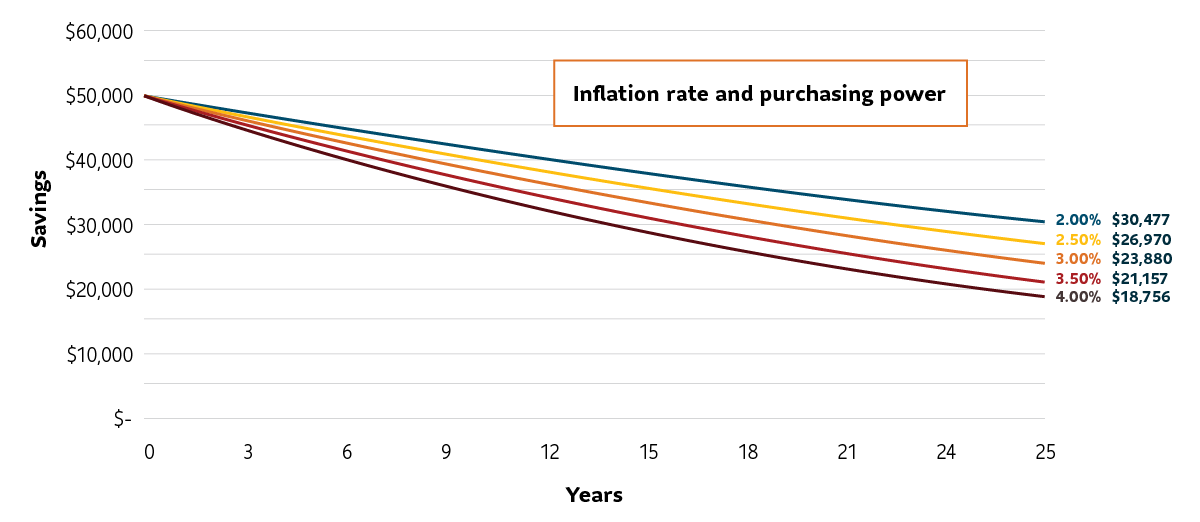

Inflation is an economic environment in which the cost of goods and services rises and the value of purchasing power falls. An increase in inflation can be caused by many things, including supply shortages, rising demand for goods, or rising production costs. Inflationary pressure on retirees who live on a fixed income is a challenge that can threaten to derail their retirement plans because their purchasing power steadily declines over time. Add to this a market downturn and it can be difficult, if not impossible, for a portfolio to achieve the growth it needs to keep pace with or even mitigate inflation.

In the chart below, look at how a sample client’s purchasing power is reduced by rising inflation.

Source: Sun Life Global Investments. Inflation rates used are hypothetical*. Source: Bank of Canada Inflation Calculator.

Liquidity, or easy access to one’s money, is a key retirement need. The amount of liquid assets needed will vary by client, but having them is a must for emergencies and unexpected expenses. Further, liquidity is key in helping to fund retirement lifestyle expenses. Think about things that your clients enjoy, like golf and other hobbies, gifts, and travel.

If you don’t factor in liquidity risk when creating retirement income portfolios for clients, you’re leaving them vulnerable to having to cash in on other investments, which could come at a cost, such as the decreased value of the guarantees associated with a segregated fund contract, or the market value adjustment made when a GIC is accessed prior to maturity.

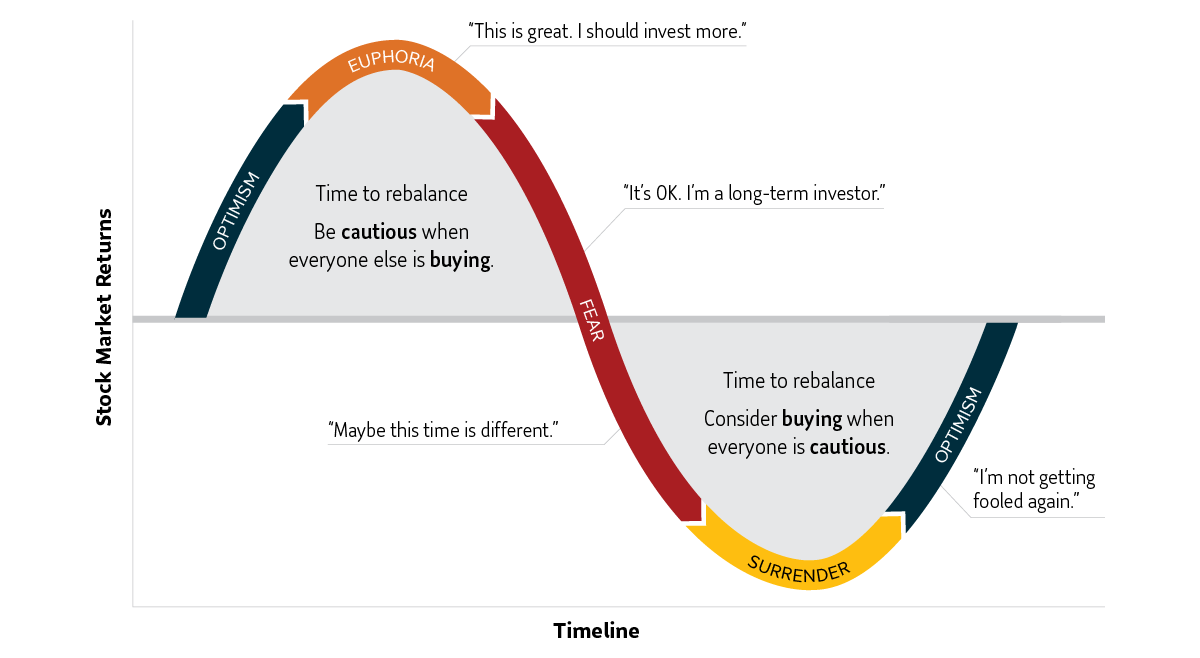

Behavioural risk refers to the likelihood of a client making investment decisions that will negatively impact their portfolio either in the short or long-term. An example would be a knee-jerk reaction to a market downturn when the client wishes to immediately move money out of an investment that has decreased in value. Doing so would crystalize their investment loss. Behavioural risk is an important factor to consider in creating retirement income portfolios. Knowing beforehand how clients could react in the face of a sudden market downturn could be helpful in being able to recommend the right income generating products.

Market cycle of emotions

How some investors may feel during a typical market cycle

Source: Forbes (with adaptations).

While estate planning is critical for any client regardless of life stage, it becomes even more important as they age. A client dying intestate – without a valid will – means their assets may be subject to probate, which can be a time consuming and expensive process. Probate fees can reduce the value of the estate. Further, a court will usually make the details of an estate a matter of public record. This means the deceased’s privacy could be lost and beneficiaries and vulnerable heirs could become targets for financial abuse.

Further, dementia is on the rise. With 1.7 million Canadians expected to be living with dementia by 20502, there’s a good chance you’ll encounter clients with some form of this condition. It’s critical to have estate planning conversations with aging clients as soon as possible. Otherwise, they could be left without an estate plan in place before they become cognitively incapacitated. If you have clients near or in retirement who don’t yet have estate plans in place, now is the time to have estate planning conversations with them.

How can Product Allocation help address all of these needs and risks?

The goal of Product Allocation is to help ensure that all of the needs and risks outlined above are addressed in varying degrees according to client preference. Product Allocation can accomplish this difficult task because it proposes the use of more than one income generating product in a retirement income portfolio, in order to obtain an array of features and benefits. No one product can offer the protection needed to cover all needs and risks. Product allocations will differ by client, in line with what each unique situation requires.

Life annuities have been around for many years. A simple, conservative investment, they provide guaranteed income for life, and are not affected by market volatility. Dollar for dollar of premium, Life Annuities are among the most cost-effective ways to address longevity risk. This means they can be an ideal product to help cover basic expenses. A Life Annuity can supplement other sources of guaranteed income, such as the Canada or Quebec Pension Plan (CPP or QPP), Old Age Security (OAS), or a defined benefit pension plan.

As insurance contracts, Life Annuities provide other benefits too, such as the ability to name beneficiaries.3 With a named beneficiary in place, a death benefit can be paid out without the time, expense, and scrutiny of the probate process when the annuitant dies. This can help make for a more efficient estate settlement. Further, a vulnerable beneficiary is protected from potential financial abuse.

Payout annuity resources from Sun Life Global Investments:

Sun Life Global Investments’ Payout Annuity options

Life Annuities aside, guaranteed interest products fall into two camps:

GICs are reliable deposit products and have been available in Canada for a very long time. Both types of GICs can be converted into income generating products for retirement. Maturity dates can be laddered (staggered) to create a consistent stream of income or to align with planned expenses.

Insurance GICs offer additional benefits that trust/bank GICs do not. This includes the ability to name a beneficiary on non-registered assets, thereby providing estate planning benefits, such as bypass of probate.

Insurance and Trust GIC resources from Sun Life Global Investments:

Adding a segregated fund contract, or guaranteed investment fund (GIF), to a retirement income portfolio can help address many retirement risks and needs.

In addition to providing growth through underlying investments and capital preservation through guarantees, some contracts may offer a reset feature on the death benefit guarantee. This serves to lock in market growth, further protecting these assets from future market downturns. Market volatility and sequence of returns risk, along with inflation, effectively can be managed through these features.

As an insurance contract, a GIF can provide estate planning advantages, such as bypass of probate. It does this through the ability to name beneficiaries. Beneficiaries will receive a guaranteed amount (between 75% and 100%) or the market value of the contract, whichever is greater.

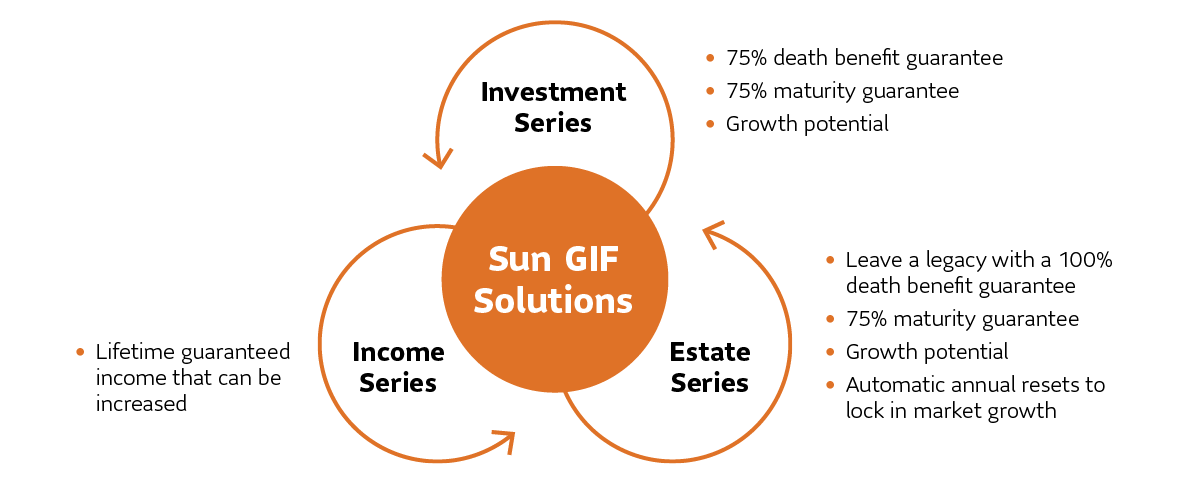

It’s also possible for GIF contracts to offer different “series” of underlying mutual funds that can help meet evolving financial needs at different life stages. One series of mutual funds may have lower management expense ratios (MERs) with lower death and maturity benefit guarantees (for example 75%/75%). A client can start in this series and later move into another series that offers more robust guarantees as their life needs change. Some GIFs offer a series that provides lifetime guaranteed income. If a client invests in the income series and in other series offered by the GIF, they can increase their lifetime guaranteed income by moving assets into the income series from the other series. This may help to offset inflation and fund basic expenses. Further, it may help to mitigate longevity risk.

Sun GIF Solutions, a segregated fund contract available from Sun Life Global Investments:

Segregated fund resources from Sun Life Global Investments:

Sun GIF Solutions, offering lifetime guaranteed income

Sun GIF Solutions Estate Series, with a 100% death benefit guarantee and automatic annual resets

Sun Life GIFs Proposal tool (log in required)

Information on taxation of segregated fund contracts:

The sky’s the limit when it comes to mutual fund investing, with thousands of funds that invest in virtually every asset class. Further, mutual funds aren’t just for clients in their accumulation years; they’re for retiring clients too. This is because they can be liquid, provide growth and, depending on the fund, offer capital preservation. Importantly, they can also pay a consistent, tax efficient income.

In allocating some assets to mutual funds, a portion of a retiree’s portfolio would have the flexibility to fund lifestyle expenses and manage financial emergencies. It would also have the ability to continue growing while they’re drawing income from other investments. This growth may help the overall portfolio to keep pace with or mitigate the effects of inflation.

A systematic withdrawal plan can be set up on a mutual fund to create regular income. What’s more, some mutual funds pay monthly distributions, which can also provide a consistent source of income. These capabilities and the growth they offer may make mutual funds a useful means of providing retirement income, in combination with guaranteed income generating products.

Mutual fund resources from Sun Life Global Investments:

Sun Life Global Investments’ mutual fund options

Discover Sun Life MFS Funds, offering growth and income-oriented funds

Selling an investment at a lost to receive a tax benefit: pitfalls to avoid

Next steps in moving to a Product Allocation approach for retirement income

The goal of Product Allocation is to help ensure that a retiree’s unique needs and the risks that are most concerning to them are addressed, such as:

Using more than one income generating product is critical because no one product can solve for all of these retirement needs and risks.

So, what are your next steps towards building Product Allocation strategies for clients? It starts with new conversations about:

These points can help you determine what income generating products might work best for each client and what portion of their assets should be placed into each product.

In addition to these important conversations, you can also visit the following to learn more about our featured retirement income solutions:

Solve for more dimensions of risk with a multi-product strategy

1 CNBC Personal Finance, January 12, 2021.

2 Alzheimer Society of Canada study: “Navigating the path forward for dementia in Canada,” September 2022.

3 Named beneficiaries are possible with an annuity contract when a guaranteed period is chosen.

Content pertaining to case studies, scenarios, and/or illustrations is provided for information purposes only and is not intended to provide specific individual financial, investment, tax, accounting or legal advice and should not be relied upon in that regard and does not constitute a specific offer to buy and/or sell securities. Information contained in this document has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made with respected to its timeliness or accuracy. Case studies presented are hypothetical in nature and are not intended to be representative of actual client scenarios. Each client will have individual personal income or tax situations that may have additional complexities outside the scope of materials discussed in this document. Investors should seek professional investment advice and/or the advice of a tax advisor for a comprehensive review of their personal situation prior to implementing any investment strategy.

SLGI Asset Management Inc. is the investment manager of the Sun Life family of mutual funds. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the fund’s prospectus. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Sun Life Assurance Company of Canada is the issuer of accumulation annuities (insurance GICs), payout annuities and individual variable annuity contracts (segregated fund contracts). Any amount that is allocated to a segregated fund is invested at the risk of the contract owner and may increase or decrease in value. Sun Life Financial Trust Inc. is the issuer of guaranteed investment certificates.

Sun Life Global Investments is a trade name of SLGI Asset Management Inc., Sun Life Assurance Company of Canada and Sun Life Financial Trust Inc. all of which are members of the Sun Life group of companies.